The IMO's 84th Marine Environment Protection Committee could not finalise the Net-Zero Framework, but the substance of the week was the opposite of the headline. A clear majority of member states returned to the NZF as the basis for further negotiation, reversing the adjournment that derailed MEPC.ES2 in October 2025.

Alternative proposals from Japan, Liberia, Panama and Argentina did not displace it, but made an impression that there is room for adjustment within the current framework. Alongside the NZF debate, MEPC 84 delivered the world's largest Emission Control Area, a foundational methane and nitrous oxide measurement package, and meaningful progress on the technical infrastructure the future compliance system will sit on.

The IMO Net-Zero Framework remains politically difficult. That was visible all week. But the more important shift is that most member states still see the need for a global framework, and the debate is no longer about whether shipping should decarbonise. It has moved to how the burden, the timing and the flexibility should be structured.

Without a global measure, the alternative is regional fragmentation. Different schemes, different compliance costs, different reporting systems and a less predictable investment environment. That is why the message from Cyprus, holding the EU presidency, on the need for a level playing field carried weight.

The most important data point of the week was the swing in member state positions on the NZF.

5 countries that backed adjournment at MEPC.ES2 flipped back to supporting the NZF. 10 countries that abstained or did not take a position at MEPC.ES2 now clearly support it. Only 2 countries flipped the other way, from opposing adjournment to opposing the NZF. A similar number of countries that had a clear position at MEPC.ES2 (14 supporting adjournment, 11 opposing) chose not to register a position at this meeting.

That fluidity is real, and it is a reason not to treat MEPC 85 as a foregone conclusion. But the direction of travel is clear. Alternative proposals tested the room and did not displace the NZF as the central negotiating platform.

The week opened with delegations raising seafarer safety and the operational impact of geopolitical disruptions on shipping. That was important context. The Red Sea situation and the rerouting via the Cape of Good Hope have measurably increased fuel consumption and emissions for many ships. Same cargo, same vessels, longer voyages. Industry reporting points to a 5.7% rise in global fleet fuel consumption in 2024, much of it driven by these added 7,000 to 8,000 nautical miles per voyage on affected routes.

This exposed a real weakness in the current CII framework. A ship can look less efficient on paper while the underlying operation has simply been forced onto a longer route for safety reasons. MEPC 84 therefore took up data granularity, "underway" versus "not underway" reporting, and whether future CII adjustments should better reflect weather, routing and operational realities.

Two interventions were notable.

These are not minor technical points. They go directly to the credibility of any future GHG Fuel Intensity (GFI) system.

In parallel, the GHG reduction working group, chaired by Norway, focused on the 5th IMO GHG Study: its scope, its timeline, the question of international versus domestic shipping coverage, and whether regional analysis should be included. This study will be the next major evidence base for international shipping emissions and projections, and future policy debates will increasingly depend on it.

Industry contributions added useful detail. A Brazilian company, "Marsalgado Brasil", demonstrated a fuel data tracing system, a relevant proof point as fuel certification and chain-of-custody rules become central to compliance. KCC Norway presented on why blanket measures like CII do not always fit specific operational profiles such as combination carriers, a useful reminder that decarbonisation regulation must be both ambitious and operationally workable.

By Wednesday, the NZF discussion moved into the Main Hall. The atmosphere was more diplomatic than confrontational, but the division was clear. Broadly, four groupings emerged.

Delegations not taking a clear position.

The week sharpened politically on Thursday with the Strait of Hormuz item, where a chair-approved resolution was carried in a vote of 59 in favour to 3 against. The NZF discussion itself was confirmed to push to the next session, with the question of an extraordinary session and the negotiating basis for it deferred to subsequent decisions.

Two main alternative pathways were tabled. Both helped frame the debate. Neither carried the room.

Japan moved away from the perceived "global carbon tax" character of the existing framework. It proposed:

Panama linked the GFI trajectory to the demonstrated market uptake of alternative fuels. A fuel would qualify as "commercially viable" only if it met defined thresholds.

In other words, ambition would adjust to what the fuel market actually delivers. That addresses a real industry concern. But it does so at the cost of softening the regulatory pull-through that drives that very market.

Both proposals reframe the level of ambition. Both would have softened or restructured the economic backbone of the framework. The room considered them and moved on. The signal is that alternatives may influence refinements, but the original NZF architecture remains the main negotiating platform.

The delay was not the result of one issue. Five pressures came together.

The NZF took most of the attention, but the rest of the agenda was substantive.

The NE Atlantic ECA covers the EEZs of France, Ireland, Portugal, Spain, the UK, Iceland, Greenland and the Faroe Islands. A region home to over 190 million people. It links the existing Baltic, North Sea and Mediterranean ECAs with the recently approved Norwegian Sea and Canadian Arctic ECAs, creating an almost continuous pollution control zone across the Atlantic and the Arctic.

Projected impact under a likely compliance scenario:

.png)

Implementation begins in September 2028, with stricter NOx engine limits applying to ships built from 1 January 2027. The submission was led by 27 EU member states, Iceland, the United Kingdom and the European Commission, with technical support from ICCT and Porto University.

This may be the most operationally important technical outcome of the week. For LNG and dual-fuel ships, methane slip stops being a theoretical discussion. These resolutions create the official measurement architecture on which the future GFI / NZF compliance system will sit. The numbers will feed directly into future GFI intensity calculations.

Default emission factors, chain-of-custody models, sustainable fuel certification, and the treatment of technologies such as onboard carbon capture all advanced. Future compliance will depend on the industry's ability to prove fuel origin, production pathway and well-to-wake emissions.

The next major evidence base for international shipping emissions, projections and future policy review.

MEPC 84 began the second phase of the review of short-term GHG measures, with a strong focus on strengthening SEEMP, improving operational energy efficiency, and considering whether the CII framework needs better alignment with real operational conditions, including weather and forced rerouting. It was noted, however, that at least one of the short-term measures needs to be anchored before the others can move forward efficiently.

Ballast Water Management amendments, NOx Technical Code amendments for non-carbon fuels, onboard carbon capture work, VOC measures, and marine plastic litter all progressed. Polar fuels, the global 0.5% sulphur limit and discharge from EGCS were moved into further evaluation, with potential conclusions in this session.

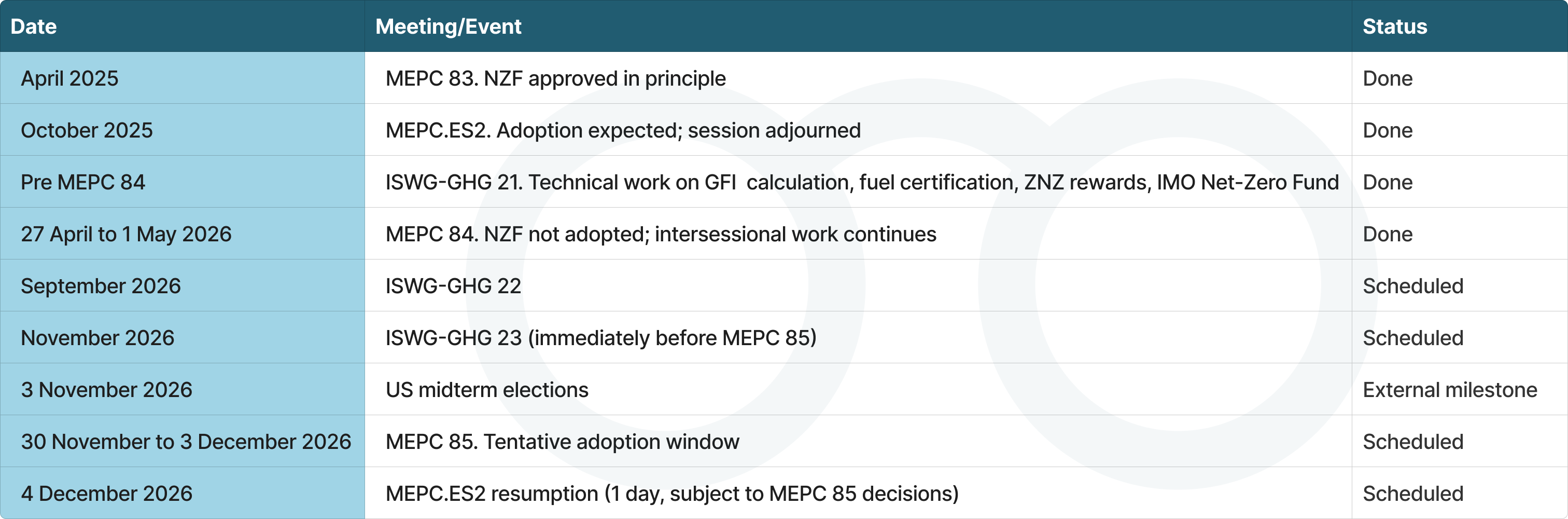

The path from MEPC 84 to a likely adoption decision is now visible.

The sequencing of MEPC 85 and the ES.2 resumption after the US midterms is deliberate, and it gives the framework a politically meaningful runway. If the NZF is adopted at MEPC 85 or the ES.2 resumption, operators will have roughly 15 months before mandatory compliance begins. Newbuilds ordered today will trade under this framework for 25 years.

The biggest mistake now would be to wait for perfect certainty.

The exact regulatory text may change. The economic element may be adjusted. The GFI trajectory may be refined. But the direction is settled. Shipping compliance is moving toward lifecycle GHG intensity, fuel traceability, operational data quality and carbon cost exposure. Companies that begin work now can still shape their options. Specifically, they can:

This is not abstract preparation. Operators that use this 18-month pre-adoption window will not just comply earlier. They will make better investment decisions, manage risk more effectively, and build credibility with cargo owners, financiers and regulators.

MEPC 84 was not the end of the Net-Zero Framework. It was the start of a more serious negotiation.

The NZF was not adopted. The conversation moved forward. Alternative proposals were tested. Technical infrastructure advanced. The majority of the debate still pointed toward convergence, not collapse.

IMO negotiations can be slow. The energy transition in shipping is not.

The window is open. It will not stay open forever.

.png)

The IMO's 84th Marine Environment Protection Committee could not finalise the Net-Zero Framework, but the substance of the week was the opposite of the headline. A clear majority of member states returned to the NZF as the basis for further negotiation, reversing the adjournment that derailed MEPC.ES2 in October 2025.

Alternative proposals from Japan, Liberia, Panama and Argentina did not displace it, but made an impression that there is room for adjustment within the current framework. Alongside the NZF debate, MEPC 84 delivered the world's largest Emission Control Area, a foundational methane and nitrous oxide measurement package, and meaningful progress on the technical infrastructure the future compliance system will sit on.

The IMO Net-Zero Framework remains politically difficult. That was visible all week. But the more important shift is that most member states still see the need for a global framework, and the debate is no longer about whether shipping should decarbonise. It has moved to how the burden, the timing and the flexibility should be structured.

Without a global measure, the alternative is regional fragmentation. Different schemes, different compliance costs, different reporting systems and a less predictable investment environment. That is why the message from Cyprus, holding the EU presidency, on the need for a level playing field carried weight.

The most important data point of the week was the swing in member state positions on the NZF.

5 countries that backed adjournment at MEPC.ES2 flipped back to supporting the NZF. 10 countries that abstained or did not take a position at MEPC.ES2 now clearly support it. Only 2 countries flipped the other way, from opposing adjournment to opposing the NZF. A similar number of countries that had a clear position at MEPC.ES2 (14 supporting adjournment, 11 opposing) chose not to register a position at this meeting.

That fluidity is real, and it is a reason not to treat MEPC 85 as a foregone conclusion. But the direction of travel is clear. Alternative proposals tested the room and did not displace the NZF as the central negotiating platform.

The week opened with delegations raising seafarer safety and the operational impact of geopolitical disruptions on shipping. That was important context. The Red Sea situation and the rerouting via the Cape of Good Hope have measurably increased fuel consumption and emissions for many ships. Same cargo, same vessels, longer voyages. Industry reporting points to a 5.7% rise in global fleet fuel consumption in 2024, much of it driven by these added 7,000 to 8,000 nautical miles per voyage on affected routes.

This exposed a real weakness in the current CII framework. A ship can look less efficient on paper while the underlying operation has simply been forced onto a longer route for safety reasons. MEPC 84 therefore took up data granularity, "underway" versus "not underway" reporting, and whether future CII adjustments should better reflect weather, routing and operational realities.

Two interventions were notable.

These are not minor technical points. They go directly to the credibility of any future GHG Fuel Intensity (GFI) system.

In parallel, the GHG reduction working group, chaired by Norway, focused on the 5th IMO GHG Study: its scope, its timeline, the question of international versus domestic shipping coverage, and whether regional analysis should be included. This study will be the next major evidence base for international shipping emissions and projections, and future policy debates will increasingly depend on it.

Industry contributions added useful detail. A Brazilian company, "Marsalgado Brasil", demonstrated a fuel data tracing system, a relevant proof point as fuel certification and chain-of-custody rules become central to compliance. KCC Norway presented on why blanket measures like CII do not always fit specific operational profiles such as combination carriers, a useful reminder that decarbonisation regulation must be both ambitious and operationally workable.

By Wednesday, the NZF discussion moved into the Main Hall. The atmosphere was more diplomatic than confrontational, but the division was clear. Broadly, four groupings emerged.

Delegations not taking a clear position.

The week sharpened politically on Thursday with the Strait of Hormuz item, where a chair-approved resolution was carried in a vote of 59 in favour to 3 against. The NZF discussion itself was confirmed to push to the next session, with the question of an extraordinary session and the negotiating basis for it deferred to subsequent decisions.

Two main alternative pathways were tabled. Both helped frame the debate. Neither carried the room.

Japan moved away from the perceived "global carbon tax" character of the existing framework. It proposed:

Panama linked the GFI trajectory to the demonstrated market uptake of alternative fuels. A fuel would qualify as "commercially viable" only if it met defined thresholds.

In other words, ambition would adjust to what the fuel market actually delivers. That addresses a real industry concern. But it does so at the cost of softening the regulatory pull-through that drives that very market.

Both proposals reframe the level of ambition. Both would have softened or restructured the economic backbone of the framework. The room considered them and moved on. The signal is that alternatives may influence refinements, but the original NZF architecture remains the main negotiating platform.

The delay was not the result of one issue. Five pressures came together.

The NZF took most of the attention, but the rest of the agenda was substantive.

The NE Atlantic ECA covers the EEZs of France, Ireland, Portugal, Spain, the UK, Iceland, Greenland and the Faroe Islands. A region home to over 190 million people. It links the existing Baltic, North Sea and Mediterranean ECAs with the recently approved Norwegian Sea and Canadian Arctic ECAs, creating an almost continuous pollution control zone across the Atlantic and the Arctic.

Projected impact under a likely compliance scenario:

Implementation begins in September 2028, with stricter NOx engine limits applying to ships built from 1 January 2027. The submission was led by 27 EU member states, Iceland, the United Kingdom and the European Commission, with technical support from ICCT and Porto University.

This may be the most operationally important technical outcome of the week. For LNG and dual-fuel ships, methane slip stops being a theoretical discussion. These resolutions create the official measurement architecture on which the future GFI / NZF compliance system will sit. The numbers will feed directly into future GFI intensity calculations.

Default emission factors, chain-of-custody models, sustainable fuel certification, and the treatment of technologies such as onboard carbon capture all advanced. Future compliance will depend on the industry's ability to prove fuel origin, production pathway and well-to-wake emissions.

The next major evidence base for international shipping emissions, projections and future policy review.

MEPC 84 began the second phase of the review of short-term GHG measures, with a strong focus on strengthening SEEMP, improving operational energy efficiency, and considering whether the CII framework needs better alignment with real operational conditions, including weather and forced rerouting. It was noted, however, that at least one of the short-term measures needs to be anchored before the others can move forward efficiently.

Ballast Water Management amendments, NOx Technical Code amendments for non-carbon fuels, onboard carbon capture work, VOC measures, and marine plastic litter all progressed. Polar fuels, the global 0.5% sulphur limit and discharge from EGCS were moved into further evaluation, with potential conclusions in this session.

The path from MEPC 84 to a likely adoption decision is now visible.

The sequencing of MEPC 85 and the ES.2 resumption after the US midterms is deliberate, and it gives the framework a politically meaningful runway. If the NZF is adopted at MEPC 85 or the ES.2 resumption, operators will have roughly 15 months before mandatory compliance begins. Newbuilds ordered today will trade under this framework for 25 years.

The biggest mistake now would be to wait for perfect certainty.

The exact regulatory text may change. The economic element may be adjusted. The GFI trajectory may be refined. But the direction is settled. Shipping compliance is moving toward lifecycle GHG intensity, fuel traceability, operational data quality and carbon cost exposure. Companies that begin work now can still shape their options. Specifically, they can:

This is not abstract preparation. Operators that use this 18-month pre-adoption window will not just comply earlier. They will make better investment decisions, manage risk more effectively, and build credibility with cargo owners, financiers and regulators.

MEPC 84 was not the end of the Net-Zero Framework. It was the start of a more serious negotiation.

The NZF was not adopted. The conversation moved forward. Alternative proposals were tested. Technical infrastructure advanced. The majority of the debate still pointed toward convergence, not collapse.

IMO negotiations can be slow. The energy transition in shipping is not.

The window is open. It will not stay open forever.