New emission levies are emerging in parts of Africa. For now, the direct cost impact is limited. But that’s not the most important takeaway.

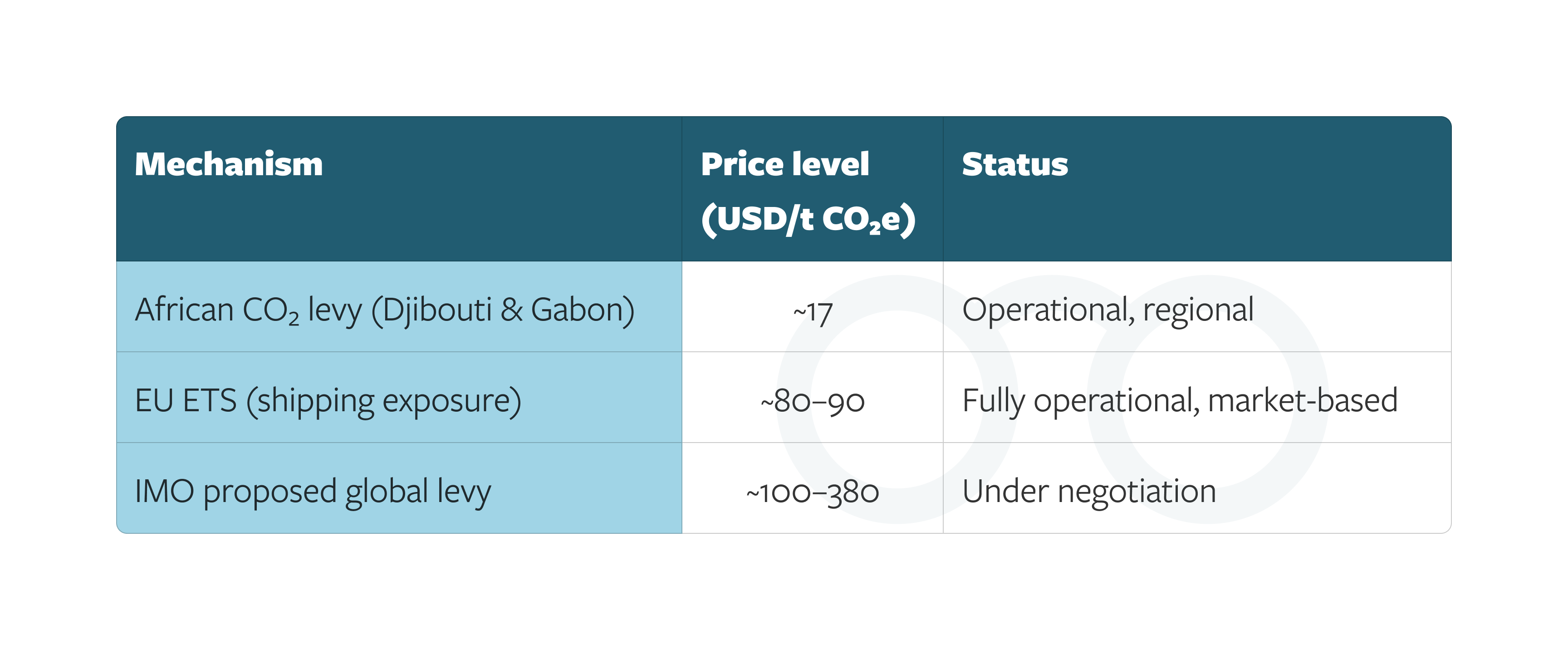

At around 17 USD per ton of CO₂e, the price is low compared to both EU ETS levels and the ranges currently being discussed at IMO. At first glance, that might make it easy to dismiss.

It shouldn’t be. This is not a weak signal. It’s a deliberate strategy. Start low to avoid resistance. Establish the system. Make it operational. And that’s exactly what we are now seeing.

The current scope is still relatively contained, but very real:

This tells us something important. The system is not broad-based. It is applied to a concentrated and repeat set of vessels and trades.

That is often how new regulatory mechanisms are introduced: focused, controlled, and operational from day one.

Even at current levels, these levies introduce something structurally new to shipping economics.

At ~17 USD per ton of CO₂e, roughly one-fifth of EU ETS levels (~88 USD), the immediate financial impact per voyage remains modest.

But they still add:

Individually, the impact is small. Collectively, it marks a shift. Because once a cost layer exists, it tends to persist and expand.

What makes these developments particularly important is not the price level, but the fact that the systems are already:

This moves carbon pricing from discussion to execution. In that sense, these levies are less about pricing emissions today, and more about proving that sovereign emissions frameworks can work in practice.

While global frameworks are still being negotiated, regional initiatives are moving ahead.

This creates a different kind of momentum, one driven not by consensus, but by implementation.

And once multiple regions begin to introduce their own mechanisms, the industry will not be dealing with a single global system, but with overlapping layers of emissions cost.

For shipping companies, the key question is no longer:

Do carbon costs matter?

But rather:

How many layers of carbon cost are we exposed to, and where?

Because today’s low-cost, localised systems may well be the foundation for broader adoption.

And the real inflection point will not come when the first levy is introduced, but when more countries follow, and the price no longer stays at 17 USD.

New emission levies are emerging in parts of Africa. For now, the direct cost impact is limited. But that’s not the most important takeaway.

At around 17 USD per ton of CO₂e, the price is low compared to both EU ETS levels and the ranges currently being discussed at IMO. At first glance, that might make it easy to dismiss.

It shouldn’t be. This is not a weak signal. It’s a deliberate strategy. Start low to avoid resistance. Establish the system. Make it operational. And that’s exactly what we are now seeing.

The current scope is still relatively contained, but very real:

This tells us something important. The system is not broad-based. It is applied to a concentrated and repeat set of vessels and trades.

That is often how new regulatory mechanisms are introduced: focused, controlled, and operational from day one.

Even at current levels, these levies introduce something structurally new to shipping economics.

At ~17 USD per ton of CO₂e, roughly one-fifth of EU ETS levels (~88 USD), the immediate financial impact per voyage remains modest.

But they still add:

Individually, the impact is small. Collectively, it marks a shift. Because once a cost layer exists, it tends to persist and expand.

What makes these developments particularly important is not the price level, but the fact that the systems are already:

This moves carbon pricing from discussion to execution. In that sense, these levies are less about pricing emissions today, and more about proving that sovereign emissions frameworks can work in practice.

While global frameworks are still being negotiated, regional initiatives are moving ahead.

This creates a different kind of momentum, one driven not by consensus, but by implementation.

And once multiple regions begin to introduce their own mechanisms, the industry will not be dealing with a single global system, but with overlapping layers of emissions cost.

For shipping companies, the key question is no longer:

Do carbon costs matter?

But rather:

How many layers of carbon cost are we exposed to, and where?

Because today’s low-cost, localised systems may well be the foundation for broader adoption.

And the real inflection point will not come when the first levy is introduced, but when more countries follow, and the price no longer stays at 17 USD.