July 28, 2021

The European Union’s “Fit for 55”-package proposes to decarbonize shipping by imposing a first-ever greenhouse gas (GHG) intensity limit on ship energy usage, a minimum tax on bunker fuels and a requirement to pay for shipping emissions in the emissions trading system (ETS) from 2023, with a full phase-in by 2026.

The union’s long-awaited “Fit for 55”-package was confirmed on the 14th July. Several measures to decarbonise the shipping industry were presented, and here is how some of the most consequential ones can impact the ship and cargo owners.

In short:

If you want more details on each initiative, keep on reading.

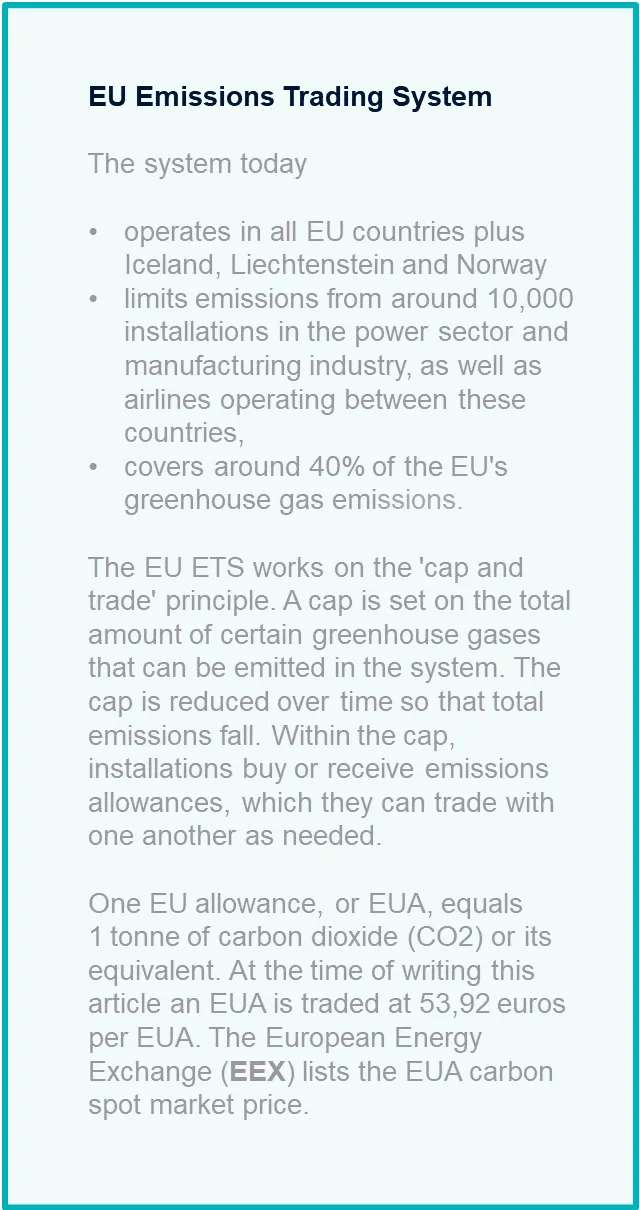

Under the new proposal shipping will be incorporated into the EU’s Emissions Trading System (ETS) (further info in fact box below) from 2023. Shipping companies will have to purchase ETS allowances for each tonne of CO2 emitted from ships operating between EU ports and at berth in EU ports, and 50% of CO2 emissions from both incoming and outgoing global EU voyages. It appears that there will be no free allowances for the maritime industry.

The measure will however be introduced in stages between 2023 and 2026. The shipping companies will only have to pay for 20% of the emissions in 2023, and requirements to surrender allowances are proposed to be phased-in as follows:

If the shipping company does not surrender the right number of allowances by April 30 of the following year, it will be fined 100 euro per tonne of CO2 not accounted for. Ships can also be denied entry to EU ports where the responsible shipping company has failed to surrender the necessary allowances for two or more consecutive years.

The entity responsible for the compliance with the ETS is the “shipping company”. In the proposed directive the shipping company is defined as the shipowner or any other organisation or person, such as the manager or the bareboat charterer, that has assumed the responsibility for the operation of the ship from the shipowner. The proposal also states that in line with the polluter pays principle, the shipping company could, by means of a contractual arrangement, hold the entity that is directly responsible for the decisions affecting the CO2 emissions of the ship accountable for the compliance costs. This entity would normally be the entity that is responsible for the choice of fuel, route and speed of the ship.

The inclusion of the polluter pays principle could make both time charterers and spot charterers responsible for the carbon cost of their commercial decisions .

To stimulate the uptake of sustainable maritime fuels and zero-emission technologies the Fuel EU Maritime proposal (further info in fact box below) sets a maximum limit on the greenhouse gas intensity of energy used on-board by a ship arriving at, staying within or departing from ports within the European Economic Area (EEA). Shipping companies will have to improve the GHG intensity of the fuels they use by

A yearly report detailing the GHG intensity of the energy used by each ship larger than 5,000 gross tonnes must be drawn up by the shipping company . The GHG intensity means the amount of CO2, CH4 and N2O emissions per MJ of energy used. It is expressed in grams of CO2 equivalent and established on a well-to-wake basis. The well-to-wake method includes not only emissions from the combustion of fuel on board the ship, but also upstream emissions from production, transport, and distribution of fuels.

A reward mechanism for overachievers allows operators using more performant technologies to exchange “excess compliance points” with less performant ships and operators. The proposal does not go into detail on this mechanism, but the impact assessment states that it would allow transfer of balance, which means buying and selling credits, between different companies.

The FuelEU proposal also addresses ships berthed at EU ports, and states that the most polluting ships (container ships and passenger ships) will be required to use on-shore power supply (or equivalent zero-emission technology). The ports will be supplied with shore-side electricity, and from 2035 and onwards vessels generally are no longer allowed to pollute when berthed at ports.

Companies that are not compliant with the rules by May 1 of the following year will have to pay penalties. The proposal states the money should be used to promote the distribution and use of renewable and low-carbon fuels.

Heavy oil used in the maritime industry will no longer be fully exempt from energy taxation for voyages in the EU. The revised Energy Taxation Directive (ETD; further info in fact box below) proposes a minimum tax on heavy fuel oil starting at 0.9 EUR per gigajoule.

In more shipping relevant terms, the 0.9 EUR/Gj tax means an additional cost of approximately 45 USD/tonne heavy fuel oil.

The minimum tax for similar fuels used in other industries is proposed at 10.75 EUR/Gj. The substantial difference in levels is described in the directive as due to the risk of shipping companies bunkering fuel outside the EU.

Some other fuels, including liquefied petroleum gas (LPG) and liquefied natural gas (LNG), will face a transitional tax rate starting at 0.6 EUR/Gj in 2023. While fossil-based, these fuels can still lend some support to decarbonisation in the short and medium term, the Commissions argues. Advanced sustainable biofuels, renewable hydrogen, and electricity will face the lowest minimum level of 0.15 EUR/Gj.

The International Maritime Organisation (IMO) efforts to reduce shipping emissions.

The EU parliament's proposal to review the monitoring, reporting and verification (MRV) Regulation.

If you want more insight into your shipping emissions profile and your future emissions exposure, please drop us a line explaining your needs.

The European Union’s “Fit for 55”-package proposes to decarbonize shipping by imposing a first-ever greenhouse gas (GHG) intensity limit on ship energy usage, a minimum tax on bunker fuels and a requirement to pay for shipping emissions in the emissions trading system (ETS) from 2023, with a full phase-in by 2026.

The union’s long-awaited “Fit for 55”-package was confirmed on the 14th July. Several measures to decarbonise the shipping industry were presented, and here is how some of the most consequential ones can impact the ship and cargo owners.

In short:

If you want more details on each initiative, keep on reading.

Under the new proposal shipping will be incorporated into the EU’s Emissions Trading System (ETS) (further info in fact box below) from 2023. Shipping companies will have to purchase ETS allowances for each tonne of CO2 emitted from ships operating between EU ports and at berth in EU ports, and 50% of CO2 emissions from both incoming and outgoing global EU voyages. It appears that there will be no free allowances for the maritime industry.

The measure will however be introduced in stages between 2023 and 2026. The shipping companies will only have to pay for 20% of the emissions in 2023, and requirements to surrender allowances are proposed to be phased-in as follows:

If the shipping company does not surrender the right number of allowances by April 30 of the following year, it will be fined 100 euro per tonne of CO2 not accounted for. Ships can also be denied entry to EU ports where the responsible shipping company has failed to surrender the necessary allowances for two or more consecutive years.

The entity responsible for the compliance with the ETS is the “shipping company”. In the proposed directive the shipping company is defined as the shipowner or any other organisation or person, such as the manager or the bareboat charterer, that has assumed the responsibility for the operation of the ship from the shipowner. The proposal also states that in line with the polluter pays principle, the shipping company could, by means of a contractual arrangement, hold the entity that is directly responsible for the decisions affecting the CO2 emissions of the ship accountable for the compliance costs. This entity would normally be the entity that is responsible for the choice of fuel, route and speed of the ship.

The inclusion of the polluter pays principle could make both time charterers and spot charterers responsible for the carbon cost of their commercial decisions .

To stimulate the uptake of sustainable maritime fuels and zero-emission technologies the Fuel EU Maritime proposal (further info in fact box below) sets a maximum limit on the greenhouse gas intensity of energy used on-board by a ship arriving at, staying within or departing from ports within the European Economic Area (EEA). Shipping companies will have to improve the GHG intensity of the fuels they use by

A yearly report detailing the GHG intensity of the energy used by each ship larger than 5,000 gross tonnes must be drawn up by the shipping company . The GHG intensity means the amount of CO2, CH4 and N2O emissions per MJ of energy used. It is expressed in grams of CO2 equivalent and established on a well-to-wake basis. The well-to-wake method includes not only emissions from the combustion of fuel on board the ship, but also upstream emissions from production, transport, and distribution of fuels.

A reward mechanism for overachievers allows operators using more performant technologies to exchange “excess compliance points” with less performant ships and operators. The proposal does not go into detail on this mechanism, but the impact assessment states that it would allow transfer of balance, which means buying and selling credits, between different companies.

The FuelEU proposal also addresses ships berthed at EU ports, and states that the most polluting ships (container ships and passenger ships) will be required to use on-shore power supply (or equivalent zero-emission technology). The ports will be supplied with shore-side electricity, and from 2035 and onwards vessels generally are no longer allowed to pollute when berthed at ports.

Companies that are not compliant with the rules by May 1 of the following year will have to pay penalties. The proposal states the money should be used to promote the distribution and use of renewable and low-carbon fuels.

Heavy oil used in the maritime industry will no longer be fully exempt from energy taxation for voyages in the EU. The revised Energy Taxation Directive (ETD; further info in fact box below) proposes a minimum tax on heavy fuel oil starting at 0.9 EUR per gigajoule.

In more shipping relevant terms, the 0.9 EUR/Gj tax means an additional cost of approximately 45 USD/tonne heavy fuel oil.

The minimum tax for similar fuels used in other industries is proposed at 10.75 EUR/Gj. The substantial difference in levels is described in the directive as due to the risk of shipping companies bunkering fuel outside the EU.

Some other fuels, including liquefied petroleum gas (LPG) and liquefied natural gas (LNG), will face a transitional tax rate starting at 0.6 EUR/Gj in 2023. While fossil-based, these fuels can still lend some support to decarbonisation in the short and medium term, the Commissions argues. Advanced sustainable biofuels, renewable hydrogen, and electricity will face the lowest minimum level of 0.15 EUR/Gj.

The International Maritime Organisation (IMO) efforts to reduce shipping emissions.

The EU parliament's proposal to review the monitoring, reporting and verification (MRV) Regulation.

If you want more insight into your shipping emissions profile and your future emissions exposure, please drop us a line explaining your needs.